Is Gap Insurance Worth It?

Gap insurance might be worth it if you're upside down on a loan or lease, however it's better to avoid it instead.

Published on January 11th, 2021. Last Updated on .

Gap insurance for automobiles is designed to provide you additional funds if your vehicle is “totaled”, and the balance of your auto loan is greater than your insurance check. While gap insurance is appropriate in some instances, you are better off just buying a vehicle that won’t put you in that position. If you need gap insurance, something (other than the accident itself) has gone wrong, and you either bought the wrong car, or got the wrong type of loan. In this article, we’ll give you advice on whether you need gap insurance, and more importantly, how to avoid situations that require it.

What is Gap Insurance?

Gap insurance, as the name implies, is there to fill in the financial “gap” if you are in a major accident and your insurance company decides that it’s less expensive to write you a check, than to have your vehicle fixed. The gap that the insurance company fills, is the difference between the amount of that check, and what you still owe on the car. For example, if your auto loan balance is $12,000 and your insurance company writes you a check for $8,000 for the total value of your vehicle, gap insurance would pay you the $4,000 difference. Gap insurance can be obtained through your existing auto insurance provider, or can be purchased separately. Here is a helpful video that explains gap insurance in detail.

What is Depreciation and Why Does it Matter?

Depreciation is the amount of value lost in an item. For a car or truck, it is the decrease in value of that vehicle over time. If you buy a car now for $20,000, and in 4 years it’s worth $8,000, it has depreciated $12,000. New cars depreciate very quickly, and it’s common for a new vehicle to lose 20% of its value in the first year it’s driven. Here’s a Depreciation Calculator that shows you just how quickly new cars lose value—or depreciate. Once a car becomes a used car, its rate of depreciation slows, but it likely never stops—unless it becomes a classic.

Depreciation is important for gap insurance purposes, as the faster your car depreciates, the more likely you are to have a gap in your insurance coverage if your car is totaled. The slower your financed car depreciates, the less you have a need for gap insurance. So, if you buy an older car for $10,000 and you put half the money down, you probably don’t need gap insurance for the $5,000 loan you took, as your vehicle will likely be worth at least $5,000 until your loan is paid in full.

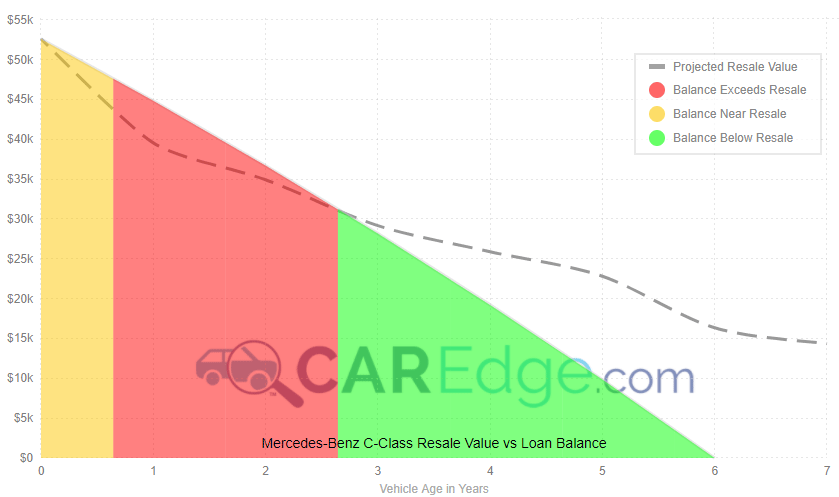

Gap Insurance is About a Race Between Your Car and Your Car Loan

A more interesting way to think about gap insurance is that it is like a race between the value of your car, and the balance on your car loan. A good outcome of the race, is that your loan’s balance never gets ahead of the value of your car. A bad outcome, is when your car loses value faster than you can pay down your car loan. We built a handy loan tool to see how your car and your loan would do in a race, and you should give it a try. What you want to achieve is to ensure that your loan is never ahead in the race. If you can avoid that (any red area on the loan tool), then you wouldn’t benefit from gap insurance, as your car would always be worth more than the balance on your loan, and there would be no “gap” to insure.

How to Avoid the Gap

It’s easy to just say “buy a car that depreciates slower”, or “make your loan balance drop faster”, but how do you do that? Listed below are a few simple rules to accomplish each objective.

To achieve slower depreciation

- Avoid buying a new car, as new cars deprecation quickly

- Avoid buying cars that are hot and trendy, as you’re probably over-paying

- Treat your cars well, and be gentle on them

- Avoid cars that will be hard to sell, or have a limited buyer audiences

- Fancy cars tend to depreciate faster than average cars

To achieve fast loan paydown

- Put as much down as you can reasonably afford, to keep the initial loan low

- Choose the shortest term loan that you can, and still make timely payments

- Pay down a loan faster than scheduled, if you get some extra cash

- Try to avoid rolling negative equity into a new loan

- The lower the interest rate, the faster you pay down loan principal

Do You Really Need Gap Insurance?

To answer this question, you really need to assess how likely it is that you’ll be upside down in your car loan, with the balance of the loan being more than what your insurance company would pay you. If you’re taking out big loans on new cars, with little money down, you have a significant chance of owing more than your car is worth. However, if you generally put 20% down or more, and pay off your cars in 5 years or less, your chances of needing gap insurance are relatively low.

Again, use our Loan Calculator, to try a number of scenarios to see how you can avoid being upside down. Our goal is to better inform you when purchasing a car, so cruise through our site, CarEdge.com to pick up tips on how to get the most from your auto investment.

Insurance rates can also differ quite a bit between providers for nearly identical coverage. If you've been with your current insurance company for more than a few years then you might be overpaying. Use our Competitive Quote Tool or the tool below to quickly compare rates. While it's free to use, we do receive a small commission if you find a better deal.